Financial Preparedness & Life Uncertainty

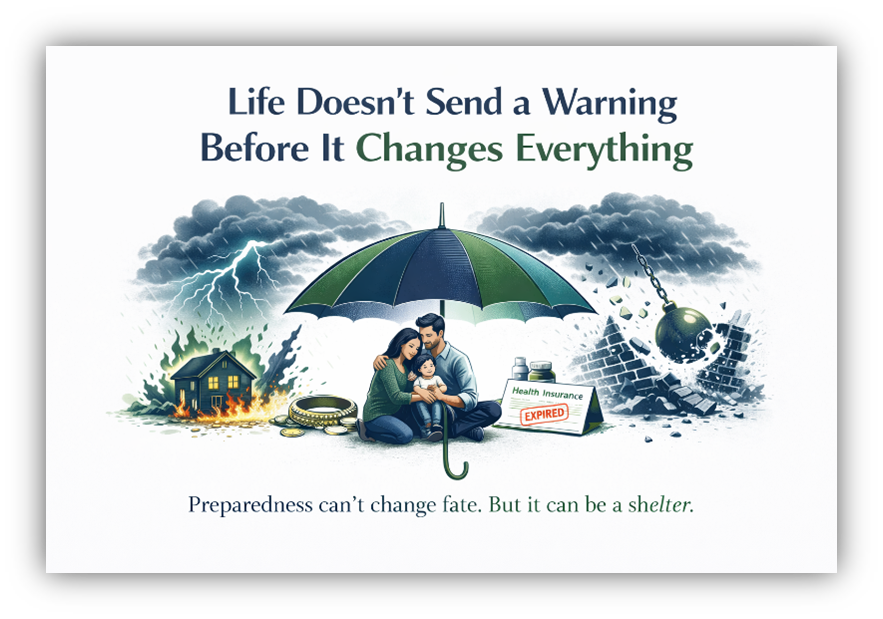

Financial preparedness won't stop the storm but it decides how hard you get hit.

There's a phone call you never expect. A diagnosis that comes out of nowhere. A job that disappears on a Tuesday afternoon. A family member who suddenly needs you financially, completely, and without warning.

None of these announce themselves. They just arrive.

And in the middle of the grief, the shock, or the exhaustion there's always a quieter crisis running alongside. The financial one. Bills that don't pause. EMIs that don't care about your circumstances. Savings that were never quite enough.

That's why this blog exists.

Why Most Financial Advice Misses the Point

Open any personal finance article today and you'll find advice about beating inflation, picking the right mutual fund, or calculating your FIRE number. All useful. But strangely silent on the question that matters most in a real crisis: will you be okay when life falls apart?

Wealth creation and financial preparedness are not the same thing. One is about growing what you have. The other is about protecting what you've built and the people who depend on it.

"The families I've seen struggle the most after a sudden loss weren't poor. They were simply unprepared. And those two things are very different."

Over the years, I've sat across from people in some of the hardest moments of their lives. Sometimes as a professional. Sometimes as a friend. And one pattern keeps showing up, again and again — the financial stress following a crisis was often not inevitable. It was a consequence of decisions made, or not made, years before.

A Story Worth Telling

REAL STORY - NAMES CHANGED FOR PRIVACY

Ramesh was 44 when he passed away unexpectedly from a cardiac arrest. He left behind a wife, two children in school, and an ageing mother. He was the sole earner.

His wife, Priya, had never managed finances independently. The house had a loan. The children's education was mid-way. Relatives stepped in initially, but that help has an expiry date.

What saved them wasn't luck. Ramesh had taken a term insurance policy eight years earlier, almost reluctantly, at his financial advisor's insistence. That one decision, a few thousand rupees a year became the difference between Priya having time to grieve and being forced into survival mode overnight.

The policy didn't bring Ramesh back. But it gave his family something irreplaceable: breathing room.

The Numbers Behind the Silence

These stories aren't rare. They're just rarely talked about in financial planning conversations.

- 77% of Indian households have no term life insurance cover

- 1 in 4 urban families have less than 3 months of emergency savings

- 68% of medical costs in India are still paid entirely out-of-pocket

- 6x higher financial stress reported in households without an emergency fund after job loss

The data points to the same gap, over and over. Not a lack of income. A lack of preparation.

What Financial Preparedness Actually Looks Like

It's not complicated. It doesn't require a large income or a financial degree. The basics, done consistently, make a disproportionate difference.

- 1. An emergency fund that actually covers emergencies. Three to six months of household expenses, sitting in a liquid account. Not locked away. Not invested. Just available. This is your first line of defence when income suddenly stops.

- 2.Term insurance while you're still healthy. The best time to buy it is when you don't feel like you need it. It is inexpensive in your 30s and increasingly expensive or unavailable if you wait for a health scare to prompt you.

- 3. Health insurance that covers the real costs. A ₹3 lakh floater policy in 2024 is not adequate. Medical inflation runs at 14% annually. Review your coverage every two to three years, not just when premiums arrive.

- 4. A family member who knows where everything is. Nominees, policy numbers, account access, passwords—someone close to you needs this information. Not someday. Now.

- 5.Long-term investing, even in small amounts. A SIP of ₹3,000 a month started at 30 becomes something meaningful by 55. The returns matter less than the discipline and the time. Staying invested through life's disruptions is what actually builds wealth.

What This Blog Is and What It Isn't

This is not a blog about predicting markets or timing investments. It will not tell you which fund to pick or when to buy gold.

It is a space for stories. Real ones. The kind that rarely make it into financial seminars or glossy magazines but that quietly shape how millions of families live through loss, illness, unemployment, and uncertainty.

Some stories will be from clients. Some from people I know. Some will be my own. All of them carry the same lesson: how you prepared, years before the crisis, determines how hard the crisis actually hits.

Fate will always have the final say. But financial preparedness decides how hard the journey feels.

Before You Go

If something happened to you tomorrow- an illness, an accident, a sudden loss of income… Would your family be okay for the next six months?

Not comfortable. Not prosperous. Just okay.

If the answer is uncertain, that's where this blog begins.